What Is Inheritance Planning?

Inheritance planning is a key part of estate planning that focuses on how your assets will be passed to your loved ones after your death.

When done properly, it:

- Makes the transfer of wealth smoother and more efficient

- Protects your family’s financial stability

- Preserves your assets for the next generation

In essence, inheritance planning helps ensure your wishes are carried out, reduces unnecessary tax exposure, and prevents complications for your family in the future.

Understanding Capital Acquisitions Tax (CAT)

CAT is a tax on gifts and inheritances. You may receive gifts and inheritances up to a set value over your lifetime before having to pay CAT. Once due, it is charged at the current rate of 33% (valid from 6 December 2012). For more information on previous rates see www.revenue.ie

- The person who gives you the gift or inheritance is called the disponer.

- The person who receives the gift or inheritance is called the beneficiary.

- Gifts become inheritances if the disponer dies within two years of giving the gift.

Capital Acquisitions Tax (CAT) — often referred to as inheritance tax or gift tax — is the tax charged when someone receives a gift or inheritance.

- Current rate: 33% (as of April 2024)

- Exemptions: Transfers between spouses and civil partners are fully exempt

Two Types of CAT

- Inheritance Tax: Applies to property or assets received after someone’s death.

- Gift Tax: Applies to assets or benefits received during a person’s lifetime.

Key Dates to Know

- Date of Gift or Inheritance:

This is usually the date the gift is received or the date of death of the person leaving the inheritance. These dates determine which tax rate and group threshold apply. - Valuation Date:

This is the date on which the value of the assets is calculated. It also determines when the tax must be paid.- If the valuation date falls between 1 January and 31 August, the pay-and-file deadline is 31 October of the same year.

- If it falls between 1 September and 31 December, the deadline is 31 October of the following year.

You pay CAT on funds from a bank, building society, An Post, credit union or other financial institution accounts. A credit union account passing under a nomination, cash, house or lands, household contents, paintings, jewellery, cars, stocks and shares, the free use of property and interest free loans, a limited interest or a right of residence in a property, a benefit received out of a discretionary trust, a further share in jointly held property that you inherited from another joint owner.

You do not pay CAT on a gift or an inheritance if either it is given to you by your spouse or civil partner or the total is below the relevant group threshold amount (when its value is added to previous gifts and inheritances in the same group). You do not pay CAT on a gift with a value of €3,000 or less from any one person in any one calendar year.

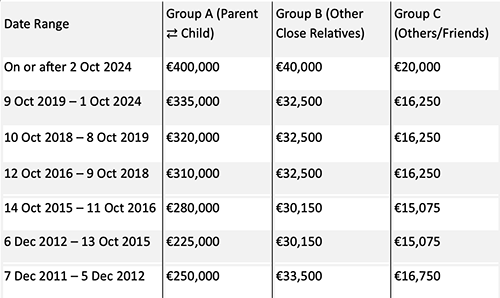

CAT Group Thresholds — How Much You Can Receive Tax-Free

You only pay CAT if the total value of gifts or inheritances you’ve received from one person exceeds your tax-free threshold.

The threshold depends on your relationship to the disponer — the closer the relationship, the higher the limit.

You must also include the taxable value of any previous gifts or inheritances received from the same group since 5 December 1991.

Understanding the Three CAT Groups

Group A – Parents and Children

This group applies mainly to gifts and inheritances between parents and children.

It includes:

- Children (including adopted and stepchildren) of the disponer or their civil partner

- Minor (under 18) grandchildren where their parent — the disponer’s child — is deceased

- Certain foster children (in specific circumstances)

- Parents inheriting an absolute interest from a deceased child

Group B – Extended Family

Applies to other close relatives, such as:

- Parents (in limited cases, e.g., when receiving a gift rather than an inheritance)

- Brothers and sisters

- Nephews and nieces (including those qualifying for “favourite nephew/niece relief”)

- Grandparents and grandchildren (where Group A doesn’t apply)

- Certain in-laws and relatives by civil partnership

In some cases, a fostered person may also qualify for Group B if receiving a gift or inheritance from:

- A relative of their foster parent, or

- Another person who was also fostered by the same foster parent.

Group C – All Other Relationships

This group applies to anyone not covered by Group A or Group B, such as:

- Uncles, aunts, cousins, in-laws, grandnephews, grandnieces, and friends.

Example:

- A nephew inheriting from an uncle = Group B

- An uncle inheriting from a nephew = Group C

In Summary

- No tax is due if the total value of gifts or inheritances from one person remains below your threshold.

- CAT is only payable on the portion above that limit.

- Closer relationships benefit from higher thresholds.

- Regular reviews and good inheritance planning can help reduce future tax exposure and ensure your estate passes smoothly to those you care about.

All information and views contained within this article is for informational purposes only and the views expressed do not constitute financial advice. U Consulting makes no representations as to the accuracy, completeness or suitability of any information and will not be liable for any errors, omissions or any losses arising from its use. Please consult a professional financial advisor before making any financial decision.

Transform your financial life

Author – Brian Flanagan

Topic – Wealth Management